How I Track Supplement Investments Without Losing My Mind

Ever poured money into nutritional supplements only to wonder if they’re actually paying off? I’ve been there—spending on vitamins, protein powders, and specialty blends, unsure whether I was boosting health or just draining my wallet. Over time, I discovered financial tools that changed everything. This is how I started tracking my supplement spending like an investment, not an expense—balancing cost, quality, and long-term value. No jargon, no hype—just real strategies that work. What began as a personal curiosity soon revealed a broader truth: when we treat wellness spending with financial discipline, we gain clarity, control, and confidence. This is not about cutting corners on health, but about making smarter, more intentional choices that align with both our bodies and our budgets.

The Hidden Cost of Health: Why Supplements Are More Than Just Monthly Expenses

Nutritional supplements often slip into our monthly routines unnoticed—another bottle added to the shopping cart, another charge on the credit card. Yet, over time, these seemingly small purchases accumulate into a significant financial commitment. For many women between 30 and 55, managing family health, personal wellness, and household budgets means juggling multiple priorities. In this balancing act, supplements can quietly become one of the largest recurring personal expenses, rivaling gym memberships or even small insurance premiums. The key insight is this: what we often label as a simple wellness expense is, in economic terms, a long-term investment in physical resilience, energy levels, and preventive care.

Consider the typical monthly spend on a basic regimen—multivitamins, omega-3s, vitamin D, probiotics, and perhaps a collagen or magnesium supplement. At an average of $60 to $100 per month, that amounts to $720 to $1,200 annually. Over a decade, that’s nearly $10,000—money that could fund a family vacation, contribute to a home renovation, or even seed a modest investment account. The opportunity cost of this spending is real. If the supplements aren’t delivering measurable benefits, or if cheaper, more effective alternatives exist, then a portion of that money is being lost—not just spent. This reframing—from expense to investment—shifts the mindset from passive consumption to active stewardship.

Treating supplements as financial commitments means asking harder questions: Is this product improving my energy, sleep, or immunity in a way that justifies its cost? Could a different brand or formulation deliver the same results for less? Am I actually using the full bottle, or is it gathering dust on the shelf? These are not just health questions; they are financial evaluations. When approached with this lens, supplement choices become more deliberate. The goal is not to eliminate spending, but to ensure every dollar contributes to a return—whether that’s fewer sick days, better mood stability, or reduced reliance on other medical interventions down the line. This mindset encourages accountability and reduces impulsive buying, especially during sales or influencer-driven trends.

Moreover, the long-term nature of supplement use mirrors other investment behaviors. Just as compound interest grows slowly but powerfully over time, the cumulative effect of consistent, high-quality supplementation can support sustained well-being. Conversely, poor choices—low-potency formulas, inconsistent use, or products with poor absorption—can lead to wasted capital and unmet health expectations. By recognizing that every purchase represents a decision point in a larger financial and health trajectory, individuals gain the power to make choices that are both economically sound and personally meaningful. This shift in perspective is the foundation for smarter, more sustainable wellness spending.

From Guesswork to Strategy: Applying Financial Tools to Daily Wellness Spending

For years, many consumers have chosen supplements based on packaging, brand familiarity, or recommendations from social media. While these sources can offer useful starting points, they rarely provide a clear financial picture. Without a structured approach, it’s easy to fall into patterns of overbuying, underusing, or selecting products that don’t deliver real value. The solution lies in applying simple financial tools to everyday wellness decisions—tools that don’t require a finance degree but do require a shift in mindset. By introducing concepts like cost-per-serving analysis, break-even timelines, and value tracking, it becomes possible to assess supplements not by their marketing claims, but by their actual performance and affordability.

One of the most effective tools is the cost-per-serving calculation. This involves dividing the total price of a supplement by the number of servings in the container. For example, a $30 bottle of fish oil with 60 capsules costs $0.50 per serving. A premium brand priced at $50 for 90 capsules comes out to about $0.56 per serving—only slightly more expensive, but potentially offering higher purity or better absorption. At first glance, the cheaper option seems superior, but when bioavailability and dosage efficiency are factored in, the more expensive product may actually provide better value. This method prevents automatic selection of the lowest price tag and encourages a more nuanced evaluation of true cost.

Another useful concept is the break-even timeline—how long it takes for a higher-quality supplement to justify its upfront cost through better results or reduced need for additional products. For instance, a well-formulated probiotic might eliminate the need for digestive aids or reduce bloating-related discomfort, leading to fewer doctor visits or over-the-counter medication purchases. By estimating these secondary savings, the initial premium price becomes easier to justify. Similarly, tracking usage patterns over time can reveal whether a product is being used consistently or abandoned after a few weeks. If a supplement sits unused for more than 30% of its shelf life, it’s effectively a financial loss—money spent on potential benefit that was never realized.

These tools transform decision-making from emotional to analytical. Instead of buying because a product feels “natural” or is labeled “doctor recommended,” consumers can evaluate based on measurable outcomes and financial efficiency. Over time, this leads to more confident purchasing, reduced waste, and better alignment between spending and results. It also builds financial literacy in an area often overlooked—personal health expenditures. When applied consistently, these strategies don’t just save money; they foster a sense of control and intentionality that extends beyond the supplement aisle.

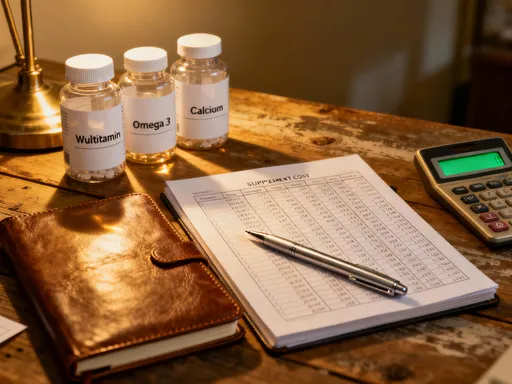

Tracking What Works: Building a Personal Supplement Ledger

One of the most powerful steps in gaining control over supplement spending is creating a personal tracking system—a supplement ledger. This doesn’t need to be complex. A simple spreadsheet, a notes app, or even a dedicated section in a budgeting tool can serve as an effective record-keeping system. The goal is to document every purchase, including the product name, brand, cost, dosage, duration of use, and any perceived effects. Over time, this ledger becomes a personalized database of what works, what doesn’t, and what’s simply taking up space.

The process begins with consistency. Each time a new supplement is introduced, it should be logged with the date of first use. Monthly check-ins allow for updates on usage frequency and observed benefits—such as improved sleep, increased energy, or reduced joint discomfort. These observations don’t need to be clinical, but they should be honest and specific. For example, instead of writing “feels better,” a more useful note might be “noticed less afternoon fatigue after two weeks of use.” This level of detail enables pattern recognition over time.

Equally important is tracking discontinuation. If a product is stopped before finishing the bottle, the reason should be recorded—was it ineffective, caused side effects, or simply forgotten? This information is crucial for identifying recurring patterns of waste. Some people discover they repeatedly buy trendy supplements during sales only to stop using them within a month. Others find that certain types of formulations—like gummies or powders—are less likely to be used consistently than capsules. These insights lead to smarter future purchases.

A well-maintained ledger also helps combat emotional buying. When faced with a flashy new product or a limited-time offer, referring back to past experiences can provide a reality check. “Did the last ‘miracle’ blend actually make a difference?” becomes a guiding question. Over time, the ledger builds a history of evidence-based decisions, reducing reliance on marketing hype. It also supports conversations with healthcare providers, offering a clear record of what has been tried and for how long. Ultimately, this system turns subjective wellness experiences into actionable financial data, empowering smarter, more confident choices.

Quality vs. Price: The Real Return on Investment in Nutritional Choices

When evaluating supplements, the most common mistake is equating low price with high value. In reality, the cheapest option often delivers the poorest return on investment. This is especially true in the supplement industry, where formulation quality, ingredient sourcing, and bioavailability vary widely. A product that costs less per bottle may require higher doses to achieve the same effect, or it may contain fillers and binders that reduce absorption. In such cases, the apparent savings are offset by inefficiency and waste. Understanding the difference between price and value is essential for making financially sound decisions.

Bioavailability—the degree to which a nutrient is absorbed and used by the body—is a critical factor in determining true cost. For example, magnesium oxide is a common and inexpensive form of magnesium, but studies show it has low absorption rates compared to forms like magnesium glycinate or malate. A person taking magnesium oxide may need to consume larger amounts to feel benefits, leading to faster depletion of the bottle and more frequent repurchases. Over time, this can make the cheaper product more expensive in terms of cost per effective dose. Similarly, vitamin D3 with added fats or oils enhances absorption, meaning the body utilizes more of each capsule, reducing the need for higher dosages.

Formulation integrity also plays a role. High-quality supplements often undergo third-party testing for purity and potency, ensuring that what’s on the label matches what’s in the bottle. While these products may carry a higher price tag, they reduce the risk of consuming contaminants or under-dosed ingredients. This is particularly important for products like fish oil, where oxidation or rancidity can diminish benefits and potentially cause harm. Brands that invest in transparency—such as publishing lab results or sourcing information—provide greater assurance of value, even if their prices are not the lowest.

Another consideration is dosage efficiency. Some supplements are formulated to deliver active ingredients in forms that require fewer daily servings. A once-daily multivitamin may cost more than a basic version requiring three pills per day, but the convenience and consistency can lead to better adherence and, therefore, better outcomes. In financial terms, this is akin to paying a small premium for a more reliable return. When evaluated over time, the higher-quality product often proves more economical because it delivers results with less waste and greater consistency. The real return on investment is not just in dollars saved, but in health outcomes achieved.

Risk Control: Avoiding Waste, Overuse, and Misguided Trends

The supplement market is filled with aggressive marketing, seasonal sales, and trending ingredients that promise dramatic results. While some innovations are backed by science, many are driven by hype rather than evidence. This environment creates financial and physical risks—overbuying, stockpiling, and consuming products that may not be necessary or safe. Risk control in supplement use involves applying the same principles used in financial portfolio management: diversification, discipline, and due diligence.

One of the most common pitfalls is buying in bulk during sales. A “buy one, get one free” offer may seem like a great deal, but if the product expires before it’s used, the second bottle represents a 100% loss. This is especially true for perishable formulations like probiotics or fish oil, which degrade over time. To avoid this, it’s important to assess actual usage rates before making bulk purchases. A simple rule of thumb: only buy as much as you can reasonably consume within six months. This prevents waste and ensures freshness.

Another risk is overuse—taking more than the recommended dose in hopes of faster results. This not only increases financial cost but can also lead to adverse effects, particularly with fat-soluble vitamins like A, D, E, and K, which accumulate in the body. Dosage discipline is essential. Sticking to evidence-based recommendations and consulting with a healthcare provider when in doubt helps maintain both safety and financial efficiency.

Finally, trend avoidance is a key component of risk management. Just because a new ingredient is trending on social media doesn’t mean it’s right for everyone. Evaluating new products through the lens of personal health goals, existing regimen, and budget prevents impulsive decisions. It’s wise to start with a single bottle, track results, and reassess before committing to long-term use. This approach mirrors dollar-cost averaging in investing—spreading out risk over time rather than making a large, speculative purchase. By applying these principles, consumers protect themselves from both financial loss and potential health complications.

When Health Meets Finance: Integrating Wellness Spending into Broader Budget Planning

Wellness spending should not exist in isolation from overall financial planning. For women managing household budgets, integrating supplement costs into a larger financial framework ensures sustainability and alignment with long-term goals. This means treating wellness as a line item in the monthly budget, just like groceries, utilities, or savings contributions. By setting a realistic allocation—such as 5% to 10% of discretionary spending—individuals can maintain consistency without overspending.

Adjusting this budget based on life stages is also important. During periods of high stress, pregnancy, or recovery from illness, supplement needs may increase, justifying a temporary rise in spending. Conversely, during times of optimal health, a simplified regimen may suffice. Regular reviews—quarterly or semi-annually—allow for adjustments based on changing needs, product effectiveness, and financial circumstances. This dynamic approach prevents rigid adherence to a regimen that may no longer serve its purpose.

Where available, using tax-advantaged accounts like Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) can further enhance the financial efficiency of supplement spending. Some medically necessary supplements, when prescribed by a healthcare provider, may qualify for reimbursement through these accounts. While over-the-counter vitamins generally do not qualify, exceptions exist for specific conditions. Consulting a tax advisor or benefits coordinator can clarify eligibility and unlock potential savings.

Additionally, aligning supplement use with preventive care strategies can reduce long-term medical costs. For example, maintaining adequate vitamin D and calcium intake may support bone health and reduce the risk of fractures later in life. While these benefits are not immediate, their financial impact over decades can be substantial. Viewing supplements as part of a proactive health strategy—rather than a reactive fix—supports both physical and financial well-being.

The Bigger Picture: Turning Smart Habits Into Lasting Financial Discipline

What begins as careful tracking of supplement spending can evolve into a broader practice of financial mindfulness. The skills developed—evaluating cost versus value, maintaining records, avoiding impulsive purchases—apply far beyond the wellness aisle. They build confidence in decision-making and foster a sense of agency over personal finances. For many, this journey starts with a single spreadsheet but leads to more intentional choices in saving, investing, and long-term planning.

The act of treating small, recurring expenses with attention and strategy creates a foundation for larger financial discipline. When individuals see the impact of consistent, informed choices in one area, they are more likely to extend those habits to other aspects of their financial lives. This ripple effect transforms personal finance from a source of stress into a tool for empowerment. It’s not about restriction, but about clarity—knowing where money goes and ensuring it serves a purpose.

Ultimately, the goal is not to eliminate spending on health, but to make it meaningful. By applying financial principles to wellness decisions, individuals gain control, reduce waste, and maximize returns—both in health and in wealth. This integrated approach reflects a deeper truth: financial health and physical health are not separate domains, but interconnected parts of a balanced life. When we care for one, we strengthen the other. And in that balance, we find not just savings, but sustainability, confidence, and peace of mind.